1 Step Forward, 2 Steps Back: What the Latest Housing Market Curveball Means for You

By Margaret Heidenry | REALTOR.COM

The housing market these days seems to meet any sign of good news with a dose of bad.

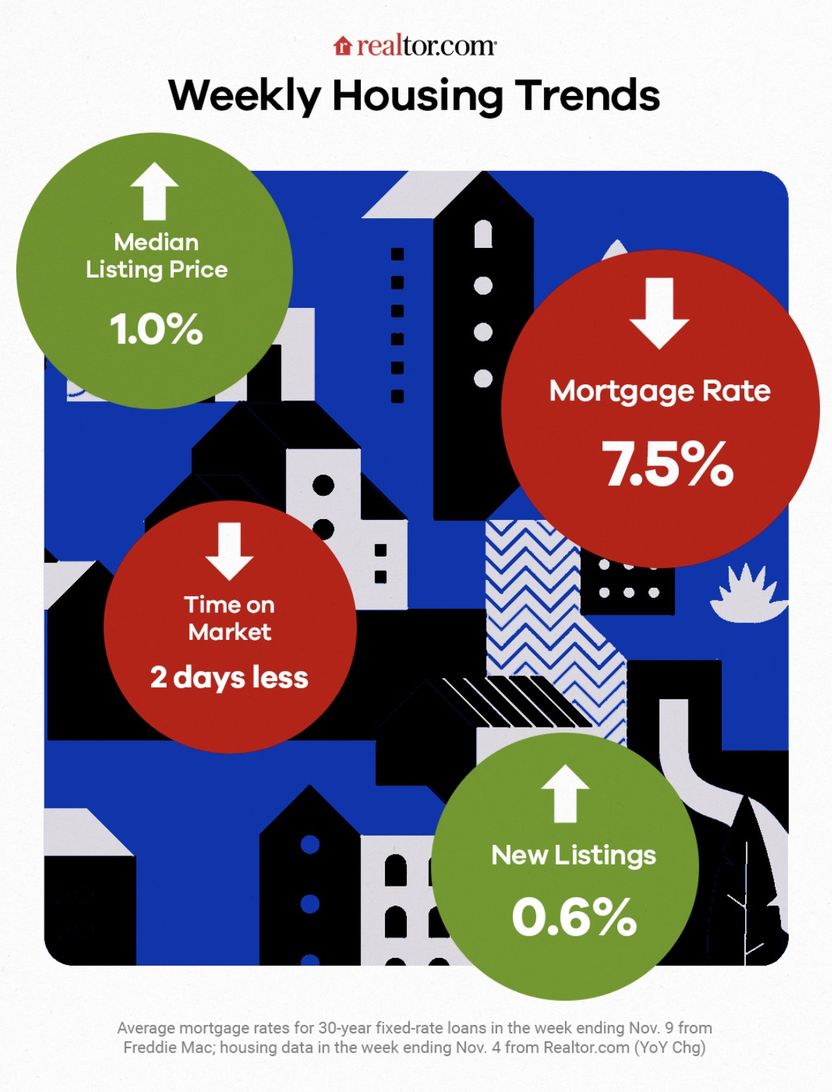

Case in point: Mortgage rates fell for the second week in a row, slipping to 7.5% for a 30-year fixed-rate mortgage as of Nov. 9. It’s a marked improvement from last week’s 7.76%, according to Freddie Mac.

While this rate dip offers a dash of relief to cash-strapped buyers, home prices marched higher for the week ending Nov. 4.

“This past week, the nation’s median listing price ticked up once again as the market continued to face tight inventory conditions,” notes Realtor.com® economic research analyst Hannah Jones in her analysis.

We’ll examine what all of the latest real estate data means for buyers and sellers in this installment of “How’s the Housing Market This Week?”

The home price squeeze

The median cost of buying a home—which averaged $425,000 in October—continues to hold the unaffordable course, rising 1.0% for the week ending Nov. 4 compared with the same week last year.

“Fairly flat or growing slightly on a year-over-year basis” is how Jones explains the holding power of unforgiving median home prices since mid-July. The budget-busting mix of high list prices and punishing mortgage rates is a recipe for an ongoing affordability crunch for the current fall housing market.

New listings tick up

In this market, any glimmer of good news is a beacon of hope, and there were some—like new listings rising 0.6% for the week ending Nov. 4.

Yet for two weeks in a row, “the trend has reversed as new listings during the week outpaced the same week in the previous year,” says Jones.

However, this slight uptick might not be enough to make an impact unless an avalanche of new listings hits the market.

Instead, “a lack of growth in new listings is likely to continue to weigh on existing-home sales in the months ahead,” says Jones.

Overall inventory continues to drag

Fresh listings might be up, but active inventory—a mix of new and old listings—shrank 0.2% for the week ending Nov. 4 in relation to last year. Or, as Jones puts it, “housing remains undersupplied.”

Active inventory has slipped for 20 weeks in a row, and the reason why remains the same: the mortgage rate lock-in effect.

This phenomenon is when current owners have an existing low-rate mortgage on their home, which shuts the door on the thought of moving—and obtaining a new, high-rate mortgage.

“Homeowners are likely to continue to choose to stay on the sidelines, limiting available inventory and propping up prices,” adds Jones.

Just how low is inventory in a historic context? “The number of for-sale homes registered 41.8% below typical pre-pandemic levels in October,” says Jones.

Limited inventory means buyers must act quickly

Yet this trifecta of high mortgage rates, high home prices, and low inventory isn’t stopping buyers from scooping up a great home when they see one.

In counterintuitive news, homes are spending two fewer days on the market for the week ending Nov. 4 than they did a year ago. (The average home spent 50 days on the market in October.) Instead, in a housing market where available homes are becoming scarcer by the day, motivated buyers seem to be wasting no time sealing the homebuying deal.

“The gap in time on market narrowed over the last few months as buyers competed over fewer homes,” explains Jones.

The mortgage rate outlook

Mortgage rates continue to be the key metric weighing down the housing market, with buyers wondering if there will be a thaw in rates this winter.

“Though [home] prices have continued to climb over last year’s level, mortgage rates have shown signs of softening following last week’s Fed meeting, promising relief for buyers,” notes Jones.

Recent employment data indicated a slowing job market, which will affect the Federal Reserve’s future rate decisions by strengthening the belief that its current policy has been effective in reducing inflation.

If future economic data further supports signs of an economic slowdown, good things might happen in the housing market.